Is VC Broken?

A win for a VC means something fundamentally different than a win for an average startup they invest in. That goal misalignment makes is behind the unhealthy relationships in the startup ecosystem.

TL;DR: Yes, VC is broken. But not for the reasons you think it is.

A disclaimer: I am officially biased. Since we extensively work with early-stage startups, it comes naturally to share their perspective whenever it departs from what VCs perceive. Whenever we need to take sides, you'll typically see me on the startup team, not the investor one.

It's then surprising to me (told you, I'm biased) how common the VC-centered perspective is when looking at the startup funding ecosystem. It’s almost as if the protagonist of that story was an investor in a venture fund.

In that story, startups are just a new incarnation of green lumber.

VC-Centered Perspective

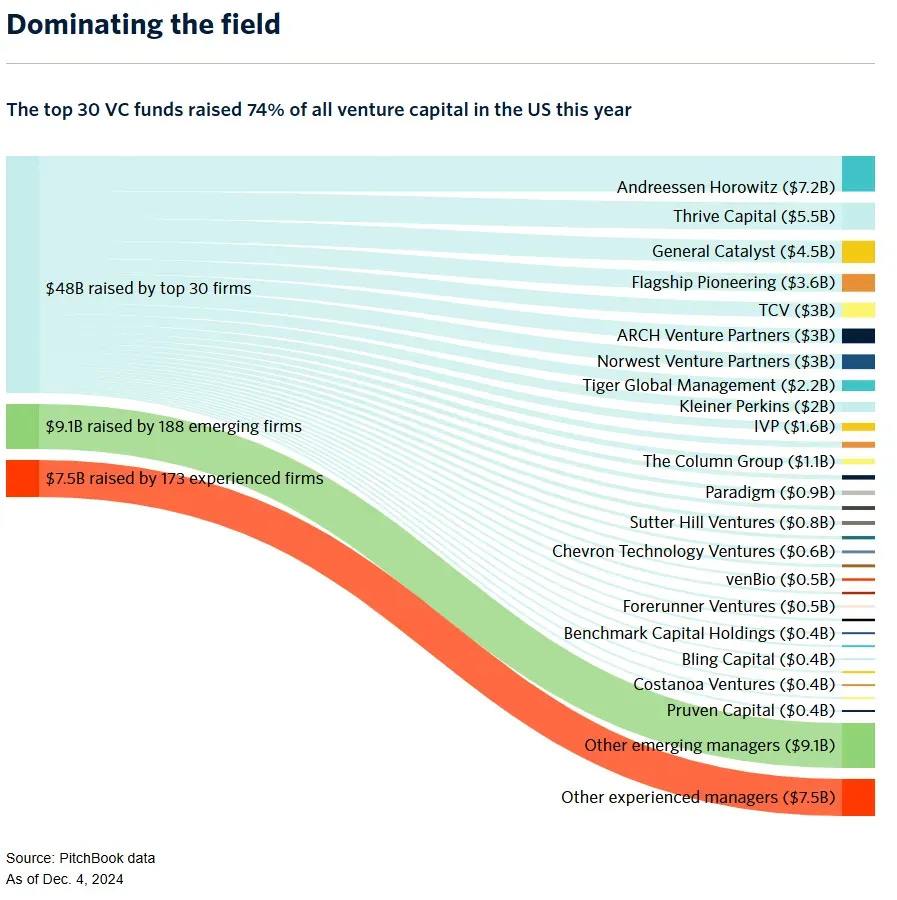

The basic narrative is a pattern of rising market concentration. Relatively few (strongest) funds have a competitive advantage in both attracting investment capital and being preferred partners by the most trending startups. The rest of the VCs are living off scraps. Figuratively, of course.

To add insult to injury, the biggest players are increasing their ambitions to enter early-stage investing, too. That section of the market was typically reserved for smaller players, angel investors, and a few prominent funds with a distinct strategy, such as Y Combinator etc.

Elisabeth Clarkson of Sapphire Partners lists all these dynamics when she asks the question about whether venture is broken. She follows up with the answer.

“No. I don't think venture is broken.

From my perspective, these are evolutions, not systemic failure. What has changed is this: Venture has gotten a whole heck of a lot harder.”

Elisabeth Clarkson

So, investing in startups becomes more challenging essentially because other VCs get fiercer and try to grab more of the market for themselves. Market concentration characteristics all the way.

Seemingly, it has nothing to do with the startup success rate (which remains unchanged, as far as we can tell) or the rise of AI (which, some enthusiasts claim, has supposedly reinvented the startup playbook). That's an interesting observation. And so VC-centered, too.

Spray and Pray Investing

Before we leave VCs entirely, let's pause on one trend as it affects startup realities. The strongest VCs have almost infinite pools of capital (and can always attract more), and they expand their operations to invest in the earlier stages of startup growth.

At the seed stage, startups still chase their Product-Market Fit. In other words, not only are we not in the growth phase yet, but we don't even know whether there will be anything to grow eventually.

Sure, the potential ROI has sweet multipliers, but the uncertainty is through the roof. It's basically a spray-and-pray tactic. Something has to grow huge eventually, right?

As a rich VC, we actually have a way of increasing the odds. If we assume that a specific business niche as a whole is a non-zero-sum game, it's enough to bet on many of the significant players. Someone will win eventually, and then we claim our spoils, whoever actually prevailed.

Oh, wait, if you look at AI and firms such as Sequoia (invested in OpenAI, xAI, Safe Superintelligence) or, even better, a16z (invested in OpenAI, Mistral, Cursor, Thinking Machines Lab), that's precisely what they are doing. It doesn't matter who wins the AI race; Sequoia and a16z will get rich.

I use the GenAI example as the most visible one, but we should expect the same tactic in just about any promising niche (which, again, the a16z example shows clearly).

If you're flush, you can bet on many horses, hypothetically even all of them. Unlike in actual horse betting, this is not a zero-sum game, which makes it an attractive opportunity.

Betting on Horse Racing Sucks for Horses, Betting on Startups Sucks for Startups

Let's switch the optics. If you had just one racehorse, stretching it till the point when running faster at a significant risk of career-ending injury is a stupid strategy.

If you're super-lucky, you eventually triumph in that major race. For the remaining 99% of us, we'd end up with a suffering creature that will never race again.

But what if you had a couple of hundred horses? You could stretch them till physical barriers and beyond, and the statistics suggest that a couple will persevere. Not only that, thanks to the endurance they built in the process, they'll be much better equipped to win that final race.

Even better, you can pitch some of your own horses against each other in each race, increasing your odds in each individual case.

As far as a metaphor goes, a startup is a horse. A founder owns just one horse. VCs own lots of horses.

The best interest of a founder is to ensure their startup's survival. That, in turn, requires some degree of caution. A VC, in turn, wants a startup to stretch as much as it can, even at a grave risk. After all, even if one breaks, they have another hundred in reserve.

There's an apparent conflict of interest here.

Startups and VCs’ Conflict of Interest

So yes, VC is fundamentally broken. It has always been. And not because suddenly we see more market concentration with all the power plays that occur whenever we take another step closer to oligopoly.

The actual reason was that the exchange between an investor and a founder was never really aligned.

I mean, it was. As long as you were a one-in-a-thousand unicorn (actually one in a hundred thousand, but whatever). Which you were not.

A VC wants every one of their startup to race at a breakneck speed. If winning the race means 1000x or bigger returns, the failure rate doesn't matter much.

If you could double your chances of hitting the jackpot by killing half of the startups that would just break even, then it's a no-brainer. Math tells you as much.

In fact, it is actually in VCs' interest to kill the slower startups early. The worst-case scenario is that a funded company barely makes enough to come back for another round of funding, but doesn't show enough promise to return to a hockey-stick-shaped trajectory ever again (see Foursquare funding history juxtaposed with their business achievements as a good example).

Assymetric Value Exchange

A founder could fool themselves that if an investor gives them a shitload of money, they care. That VCs would run an extra mile to help them succeed.

There are two mistakes here.

One, as much as a funding round is a breathing air for a startup, capital is cheap for VCs. Especially for the richest ones, who already attract plenty of cash.

Losing on most of their investments is actually part of the game. They don't care. The value of money is vastly different for an investor and for a founder.

The same is true for VCs' time, except it's the other way around. Imagine you're an investor who invested in a couple of dozen startups. You can use your time, knowledge, expertise, connections, and insight to help them. However, your day still has only 24 hours, and you can do only as much.

Would you rather help a high-potential company that is on its way to bring you a sweet 1000x ROI, or would you go with the folks who're fighting for survival? Yeah, why would I even ask?

The value of time, again, is vastly different for an investor and a founder.

These exchanges are asymmetric. And as with all asymmetric value exchanges, investors would optimize to expend what's cheap for them (money) but would conserve the scarce resource (time).

With Funds Come Expectations

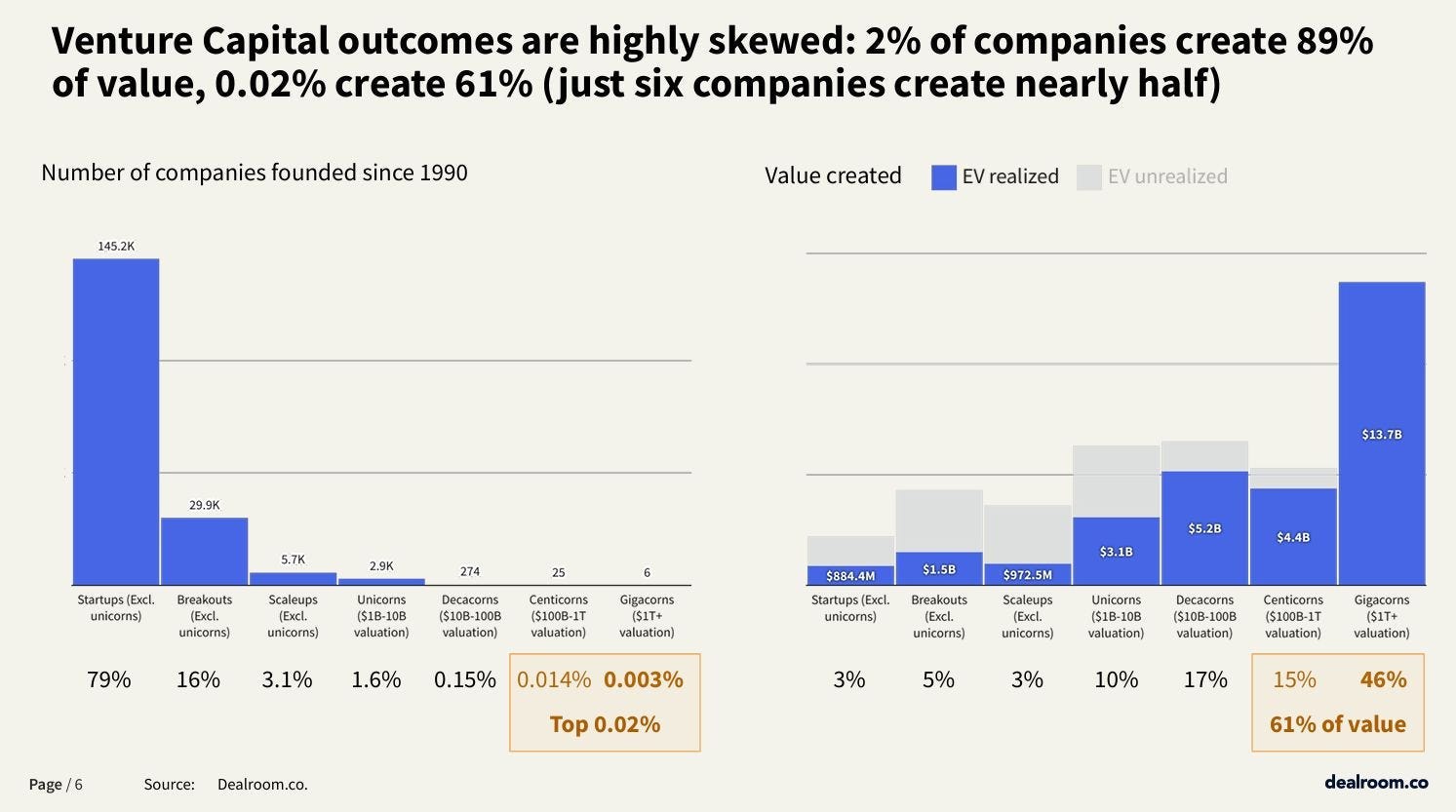

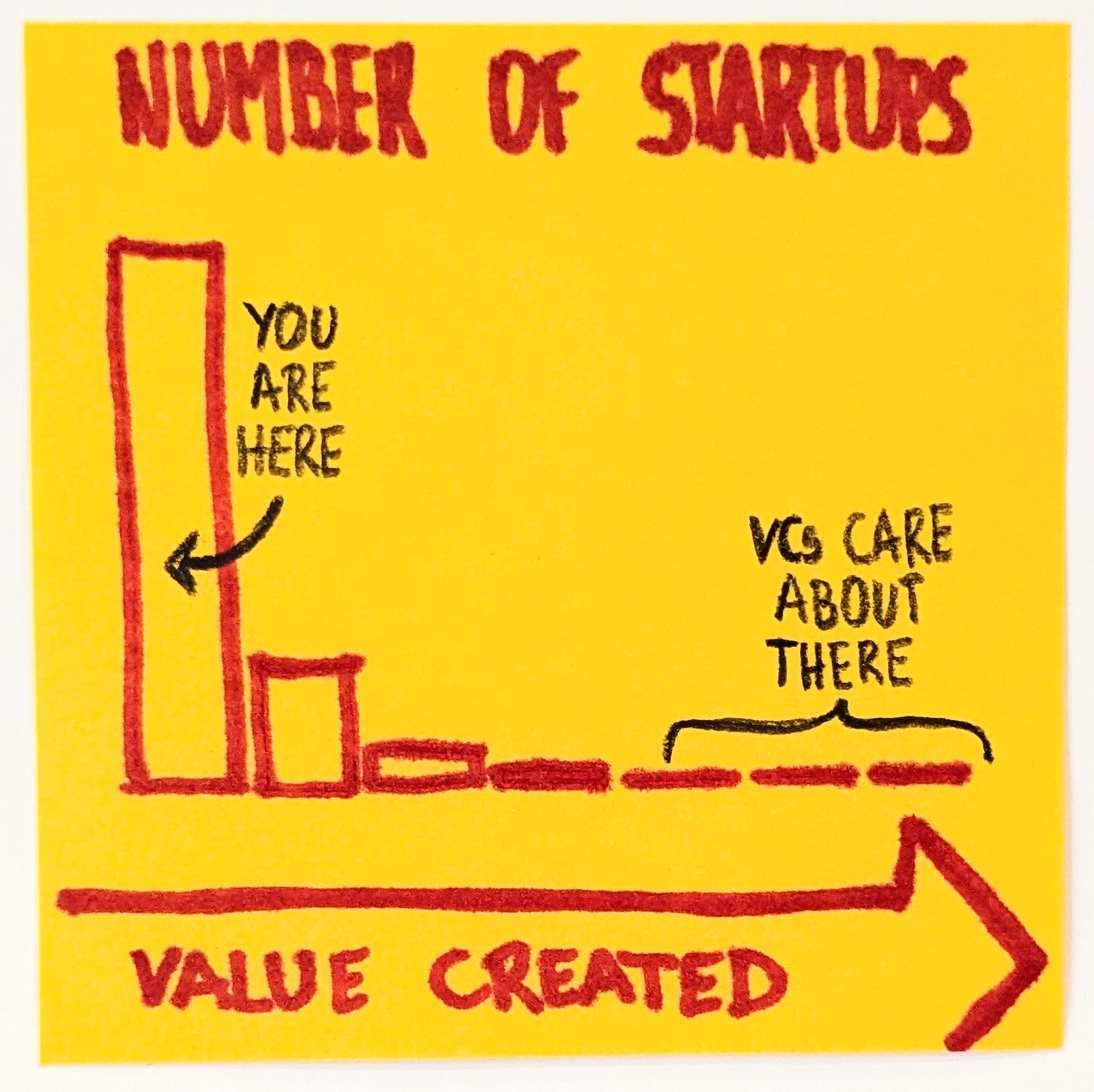

One picture is worth a thousand words. Let's then look at how investors actually make money.

Yup, about 2% of companies generate 9 out of every 10 dollars for them. Would you really expect a VC to care about a startup that's in the remaining 98%?

Now, since the rightmost part of the distribution is pretty much all the investors care about, it means that whatever targets a startup receives in a package with the funds will push them hard to the right.

Yup, you guessed it. At breakneck speed. At grave risk. No matter the cost. After all, any single startup is expendable.

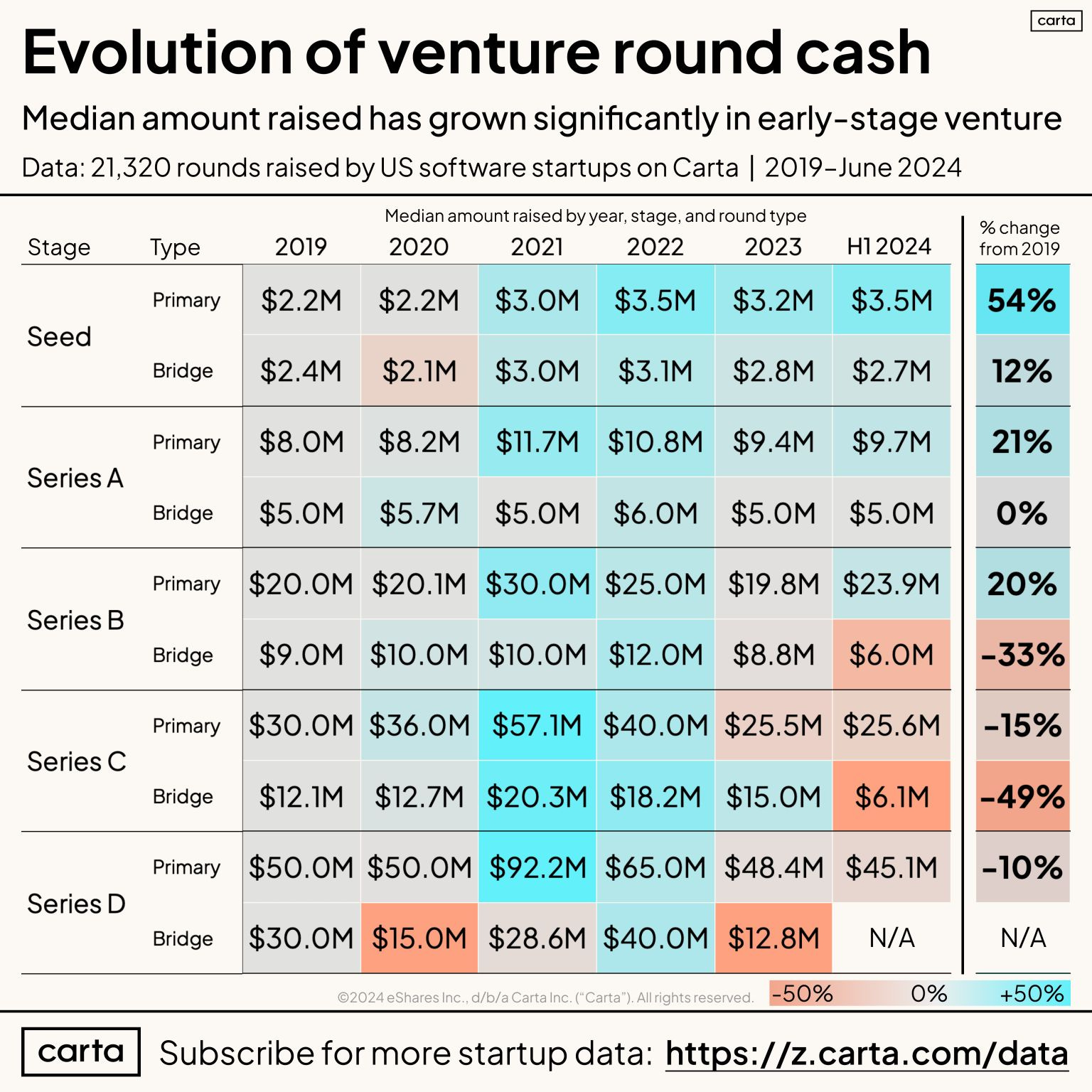

Seeing the aforementioned trend of big investors shifting to earlier funding stages, this mismatch is likely to become even more pronounced. There's no better proof of how much the pressure rises than the trend in valuation, and thus the funding rounds, of early-stage startups.

If these firms can throw billions at OpenAI, a few hundred grand of a seed round is not even like pocket money for them. I mean, they could literally spend an equal amount on seed rounds for some 12 thousand startups.

It's not unreasonable to expect that one of such startups would be the next centicorn (or whatever fancy label we use for absurdly high-valued companies). Especially if we pushed them hard enough.

The only problem? Funding 12,000 companies is so much more work than handing over all that money to Sam Altman. Still, the attitude and expectations will remain the same, regardless of how potentially harmful they may be for startups.

Because the win for a VC means something fundamentally different than a win for an average startup they invest in. The goals are misaligned.

That's why VC is broken. It has always been.

Here's a take on how to dodge the bullet and avoid playing the game altogether.