The Pre-Pre-Seed Chasm

The transition from the dream to a funded endeavor is the toughest and (typically) lethal

The funding cycle for a successful startup typically follows a similar pattern.

The dream

Pre-seed

Seed

Series A

Following Series (B, C, etc.)

IPO

Now, I don't say it's the only path, and we'll come back to it later, but that's what the startup industry wants us to be the most desirable way. After all, the follow-up to that is: "7. I'm rich!"

The Dream

Admittedly, I depart from the commonly accepted lingo with the first item on the list—the dream. At this stage, a founder is not yet ready to show their idea to the world and pitch for funding.

They use whatever resources they can scrounge—most notably, their time—and bootstrap their way until they feel ready for the next step. When it comes to available funds, we talk about anything from 0 to 5 digits.

Why not call it bootstrapping, then? I chose "the dream" because bootstrapping suggests a commitment to a different path in scaling the endeavor.

It assumes that we don't apply for an external investment or delay such a decision to a much later stage. The end goals are dissimilar, too. There's a much higher chance that a founder aspires to build a sustainable enterprise and not go IPO and get rich.

The cycle would rather be the following:

The Dream

Bootstrapping

Either one:

Sustainable business

Eventually getting money and switching tracks to the default/investment scenario

In both cases, the earliest stage—the dream—will be somewhat similar. It will be a combination of aspirations, hopes, and struggles when the hopes don't turn into reality. The paths diverge later.

The Choice

Taking on investments means jumping on a "fast growth" bandwagon. Even if it weren't the founder's intention, the pressure coming from the investors would push them down that avenue.

Sticking with bootstrapping, on the other hand, means dodging the "go bold, grow fast" bullet but creating a cash-strapped environment instead. Balancing development with the revenues will be the primary source of concern.

Interestingly enough, the investment path is a viable option when someone starts with bootstrapping and gets more successful than expected. By the same token, the latter may be a perfect fallback scenario when one fails to secure early funding to keep up with the growth path.

Before that fork in the road happens, all the aspiring founders are dreamers.

And their dreams are likely to be shattered.

The Failure

That's a point where I should play the "90% of startups fail" argument, which, by the way, is often pulled out of thin air. There's so much vagueness in the definitions (What is a startup? What is failure?) that you could make the numbers look as bad as you want. It’s easy to find articles that contradict themselves on that account. However, we can probably agree that many new endeavors do, indeed, fail. The founders play against the odds.

Most likely, they will fail at the dream stage.

In fact, the failure rate of the dreamers is underestimated. Many of them will give up before establishing any formal entity and, thus, will evade all the official statistics. Consider all those who hustle to turn their idea into something but ultimately fail before it becomes anything more than an after-hours pet project.

When the dreamers eventually give up, it's a silent failure. There hasn't yet been anyone who invested money in them. No one yet cares. They fail because they have neither reached a sustainability point (which would allow them to keep bootstrapping) nor secured a round of funding (which would extend their runway).

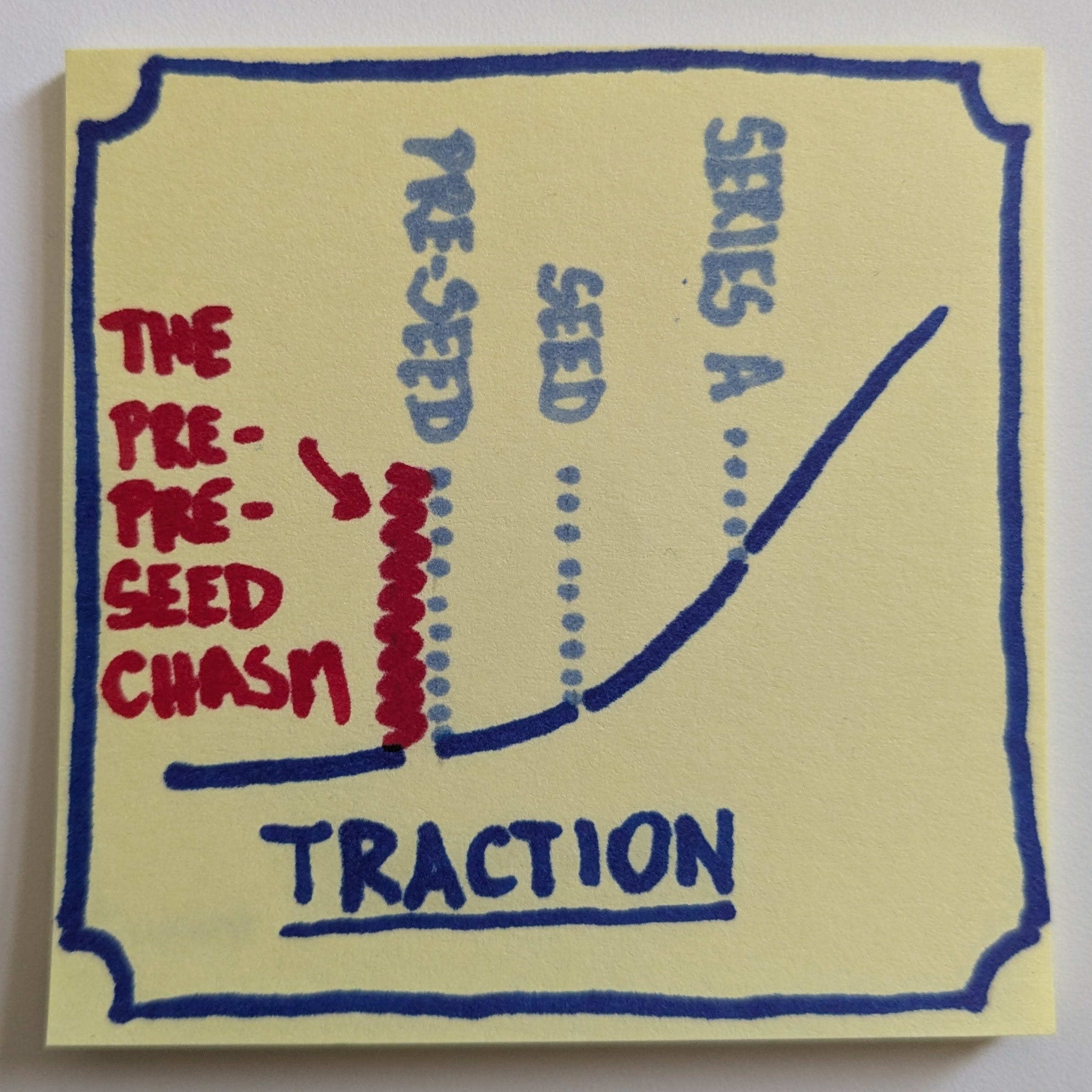

It's the first and the biggest chasm a striving startup faces.

The Transitions

I borrow the language from Geoffrey A. Moore's Crossing the Chasm here. While Moore's model has been disputed, it provides a neat metaphor. Startups, as much as new products and services, go through a maturity curve, shifting through stages at which they need to adopt different strategies. Because of the required changes, each shift is a challenge. The one retargeting the offering from the early adopters to the early majority is especially demanding, thus, the chasm.

By the same token, a startup going from the dream to the pre-seed, seed, round A, and then further rounds, each time, needs to adjust what they show up with. They need to provide an answer to increasingly more challenging questions. After all, step by step, they evolve from a hypothetical idea to a proven, profitable, proliferating business.

The most formidable transition is the first, from the dream to the first funding. Or sustainability, which acts like self-funding in this case.

It's the graduation from no one but the founders believing in the idea to some people betting their own money on it—as much the pre-seed investors as the earliest adopters (paying with their money, data, time, or all at once). The former won't happen without the latter.

Since that transition happens before the pre-seed funding round, I'll go with the name of the pre-pre-seed chasm to label it.

The Pre-Pre-Seed Chasm

The pre-pre-seed chasm is so tough to overcome because of several contradicting goals.

1. Limited runway

Whatever funds are available for the dreamers are, by definition, minimal, and the needs are plenty. Starting from sustaining basic founders' needs, through any external tools the product requires, to purchasing services beyond the immediate skills of the founding team, all these require money. Each dent in the available budget shortens the time left before the chasm becomes a gaping abyss just in front of the startup.

2. Validation

While aspiring entrepreneurs fight the closing time window, they need to attract enough early adopters to provide the early validation of the idea. As much as they can be dreamers initially, without enough traction, they won't cross the pre-pre-seed chasm. Sure, there are options to help with the growth by throwing money at the problem, but that's one thing founders don't have now.

3. Funding

As if navigating the financials and idea validation wasn't enough, getting funding is another game altogether. It eats up time and energy that the entrepreneurs might have used to work on the idea. It requires skills (preparing pitch decks, pitching, learning how to talk with the investors) that aren't otherwise useful to the startup development. It's like the entrance fee one has to pay to have a shot at getting an investment.

4. Experience (or lack thereof)

The majority of founders are first-time entrepreneurs. Oftentimes, they approach the domain they know only partially, e.g., subject domain experts, but they have never participated in building a digital product. Developing a digital product is a minefield of potentially fatal decisions. While admittedly, it's anecdotal evidence, our experience in contributing to building around 200 products shows that even second-time or third-time founders fall into many of these traps. Given the limited resources, each mistake heavily exhausts the remaining runway. Many are downright fatal.

It's almost like all forces conspired to prevent a fledgling startup from making it to the second chapter.

While there's a lot the dreamers can do differently to improve their startups' chances of survival, the first crucial step is acknowledging the pre-pre-seed chasm. What naturally follows is the changing of the perspective. Instead of aiming for exponential growth and multimillion-dollar investments, they had better concentrate on surviving to keep playing the game next quarter or year.

The big dreams won't materialize unless they can achieve at least that much.